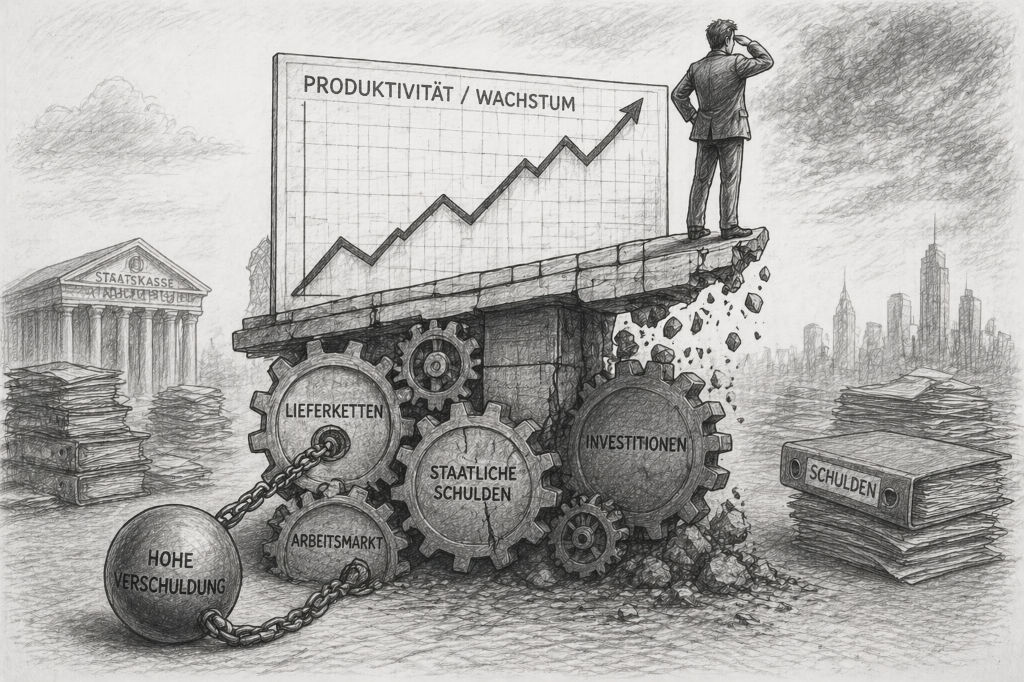

Even during the coronavirus pandemic, many economists were surprisingly unanimous: the great danger was a phase of low inflation, perhaps even deflation. A few years later, the picture is different. Inflation reached historic highs in many countries, supply chains collapsed and economic developments turned out differently than expected.

The pandemic was not just a health crisis - it was also a stress test for economic forecasts. This article shows where experts were wrong, why this was the case and what lessons can be learned for future assessments.

More than three years after the COVID pandemic shook the global economy, experts are still grappling with the question of why so many forecasts turned out to be wrong. The pandemic has led to lost sales in most industries, and entire nations are still struggling to regain their former position. In these uncertain times, economists tried to make predictions about inflation, productivity and growth. Today, many experts note that a strikingly high proportion of predictions were inaccurate. Since 55 % of the population Distrusting economists' forecasts, serious concerns arise about their methodology and application, revealing the limitations of economic forecasting in times of extreme change. With this in mind, I will analyze and summarize the accuracy of historical forecasts below.

Inflation trends

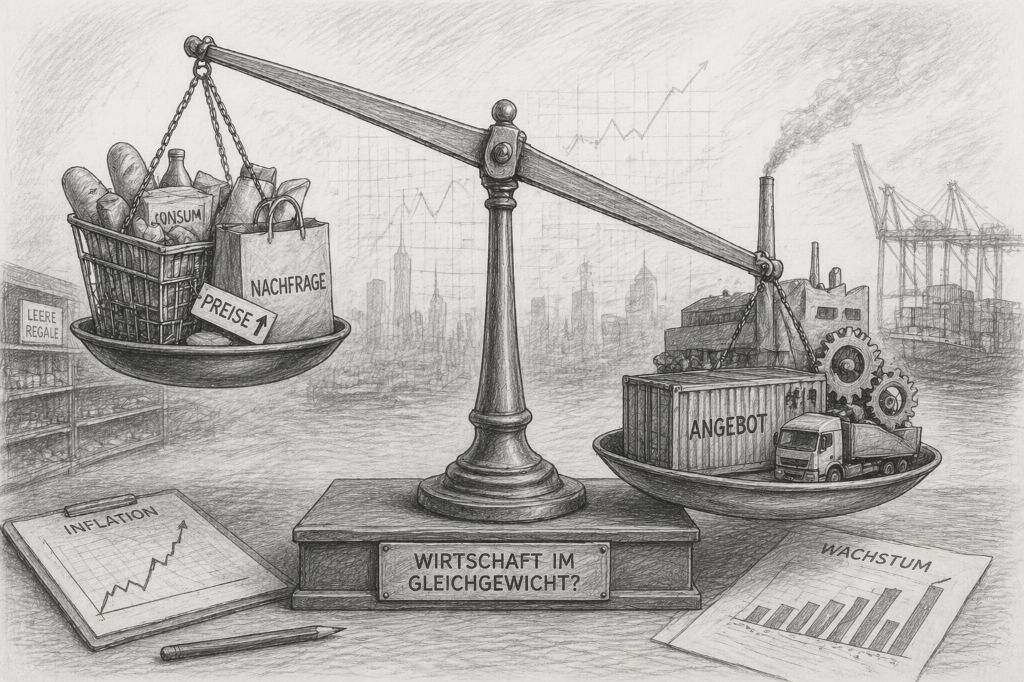

The development of inflation is one of the areas in which the uncertainty of economic forecasts has become particularly apparent. Hardly any other topic has been discussed so intensively during the pandemic - and at the same time assessed so differently.

One key aspect that many experts focused on was inflation. Although it was debated whether the pandemic would lead to higher, lower or even deflation, most experts actually agreed that the latter would occur. Many economists explained this with higher unemployment, which would limit wage growth and lead to higher savings.

A minority of economists took a more critical stance and warned against underestimating inflation risks. According to Olivier Blanchard PIIE article from the year 2020 high inflation was unlikely and would only occur in the rare event that three specific factors were present at the same time: consistent government debt, investors demanding higher interest rates and government pressure on central banks to keep interest rates low. Although Blanchard put the probability at less than 3 %, the improbable became a reality in many countries.

Current survey on trust in politics and the media

With an average inflation rate of 8 %, the USA reached its highest level since the early 1980s. This was mainly due to disruptions in supply chains. In particular, lockdowns forced many factories to close, which led to uncertainty in economic activity and resulted in production losses for various industrial goods.

Another factor contributing to higher inflation was sudden changes in consumer preferences. During the pandemic, many households cut their spending on non-essential goods. It is estimated that the pandemic was responsible for a decrease in usual household spending by about one fifth responsible. When the lockdown ended, there was a huge increase in demand for many new, typically industrially manufactured products.

Looking back, it is clear that several developments had an impact at the same time: disrupted supply chains, government intervention, changes in consumer behavior and an overall high level of uncertainty. It was precisely this combination that was underestimated in many forecasts. The development of inflation during and after the pandemic thus illustrates how difficult it is to reliably predict economic dynamics under exceptional conditions.

Economic growth

When it comes to economic growth, it also became clear early on how difficult it is to make reliable forecasts under exceptional conditions. Many assumptions initially seemed plausible - but only partially stood up to actual developments. Although it was not assumed that GDP growth would remain constant, many economists speculated on a lower long-term trend, with some controversially forecasting a sharp decline followed by a rapid recovery.

Today, most European countries are still below their pre-coronavirus pandemic trends and are experiencing slower growth than before the pandemic. One of the few exceptions in this respect is the USA, which, unlike Germany and Canada, has been back on its pre-pandemic course for some time.

In the US, the more flexible labor market has made it much easier for employees to switch between different industries. Higher spending and Investments by the population and companies supported the country's economic recovery. In addition, the USA was less exposed to external shocks than most European nations. Europe, for example, was hit hard by the attack on Ukraine and the associated energy crisis.

In the US, government measures such as extensive financial support in the form of unemployment benefits and business aid ensured a much faster recovery, while companies in other countries received significantly less support of this kind. Programs such as the Inflation Reduction Act and the CHIPS Act, both passed in 2022, ensured growth in key sectors such as domestic manufacturing and green energy through increased investment.

Overall, it is clear that economic recovery is heavily dependent on structural conditions: Labor market flexibility, government intervention and external pressures interact differently and lead to significantly divergent developments between individual regions. Forecasts that do not take sufficient account of these differences quickly reach their limits in practice.

A short article from 2021 shows how the economic impact of the pandemic was assessed differently early on than initially assumed.

Corona pandemic: German economy hit harder than expected | faz

Changes in productivity

The development of productivity was also discussed intensively during the pandemic. Many observers saw the crisis not only as a burden, but also as an opportunity for structural improvements - particularly through accelerated digitalization.

In addition, many experts believed that the COVID-19 pandemic would lead to an increase in productivity in companies, as they were forced to invest in digitalization more quickly. In fact, productivity in the second quarter of 2020 was 11.1 % higher than in the fourth quarter of 2019. However, this was partly due to the closure of lower productivity sectors, such as retail, which significantly increased the share of highly productive sectors such as finance and manufacturing.

At the same time, this increase was also driven by employees moving from sectors with low productivity to sectors with higher productivity. When the service sector reopened after the pandemic, this effect subsided again. According to an ECB analysis, the positive effect of labor reallocation in 2020 accounted for around half of total productivity growth between 2020 and 2023.

This shows how short-term productivity increases are often due to compounding effects rather than genuine efficiency gains, which many forecasts have not sufficiently taken into account.

In retrospect, this makes it clear that not every measured increase in productivity automatically indicates sustainable improvements. Particularly in exceptional situations, statistical effects can give a distorted picture if structural changes are only temporary in nature.

Debt level

Another key aspect of economic development during the pandemic was the sharp rise in debt in many countries. Hardly any other area was discussed so intensively, as short-term stabilization and long-term risks directly clashed here.

There was much debate about rising debt and the prevailing view proved to be largely correct. Many governments took on huge debts during the pandemic to fund financial measures to support the economy and prevent further collapses. It is estimated that the public debt to GDP ratio rose from 88 % in 2019 to 105 % in 2020.

Although many economists traditionally viewed higher debt as a threat to the economy, the view that higher debt can be an effective means of stabilizing entire economies gained popularity. East Asian and Pacific countries were particularly affected due to pre-existing high debt levels, with an increase of 26 percentage points of GDP. Other regions were further impacted by limited access to domestic markets, forcing governments to borrow abroad, as well as declines in output and revenues, particularly in most advanced economies and the Middle East.

Some countries in Africa recorded a significant increase in debt, mainly due to their heavy dependence on international aid and their limited fiscal space. For example, Sierra Leone's high level of debt, which was originally caused by the Ebola crisis in 2014 and 2015, continued to increase significantly due to borrowing during the COVID pandemic, which led to significant cuts in public spending.

Even though Europe was not as badly affected as many other regions, the pandemic has nevertheless caused considerable economic damage and high levels of debt and is likely to continue to restrict social spending and private sector investment.

Overall, it is clear that government debt can be a necessary instrument to ensure economic stability in times of crisis. At the same time, the long-term consequences of this development remain difficult to assess and will shape the fiscal policy scope of many countries for years to come.

| Range | Expectation of many economists | Actual development and teaching |

|---|---|---|

| Inflation | Many experts were expecting low inflation or even deflation, as unemployment and uncertainty were likely to dampen demand. | Supply chain disruptions, changes in consumer behavior and government measures led to sharp price increases. The lesson: supply bottlenecks can quickly overturn forecasts. |

| Economic growth | Many forecasts predicted a significant slump and an uncertain, in some cases weaker recovery in the long term. | The recovery varied greatly from region to region. The USA came back faster than many European countries. The lesson: the labor market, energy dependency and government support are crucial. |

| Productivity | Some experts expected digitalization and new forms of work to result in sustainable productivity gains. | Part of the increase was due to composition effects, for example due to closed sectors with lower productivity. The lesson: not every measured increase is real progress. |

| Public debt | Many economists expected a significant increase in debt as a result of extensive aid programs. | This assessment was largely confirmed. The lesson: Debt can stabilize in crises, but limits the scope for fiscal policy in the long term. |

Important findings

In summary, it can be said that many of the economic forecasts during the pandemic were only partially accurate. Although individual assumptions were not fundamentally wrong, the simultaneous impact of several factors was often underestimated. This is precisely one of the key lessons of this period.

Inflation, economic growth and productivity all showed that economic developments rarely occur in isolation. Supply chain problems, government intervention, changes in consumer behavior and structural differences between national economies interacted and led to results that were hardly ever predicted in this form. This became particularly clear in the case of inflation, the dynamics of which many models were unable to depict.

The extent to which institutional framework conditions play a role in economic growth also became apparent. Countries with more flexible labor markets and extensive government support measures were able to recover faster than others. At the same time, the development of productivity showed that short-term effects are often overestimated if they are based on statistical shifts and not on sustainable improvements.

Rising government debt, in turn, illustrates the tension between short-term stabilization and long-term sustainability. While it was an important instrument during the crisis, its future impact remains uncertain and will accompany many economies for years to come.

Overall, the pandemic makes it clear that economic forecasts reach their limits in times of profound upheaval. It underlines the importance of taking different scenarios into account and understanding uncertainty not as an exception, but as an integral part of economic reality.

A look back: where it all began

If you want to understand the economic consequences of the pandemic, there is no getting around one fundamental question: How did it all begin? While this article deals with the effects on inflation, growth and economic forecasts, it is worth taking a complementary look at the origins of the virus itself. A separate article addresses precisely this point - objectively, calmly and without jumping to conclusions. It compares the various theories on the origins of SARS-CoV-2, from natural origins to laboratory hypotheses, without evaluating any of them one-sidedly. The aim is to provide orientation and the basis for making your own judgment. Precisely because economic developments were so strongly influenced by the first months of the pandemic, this review helps to better understand the overall picture. Anyone wondering how a local health report turned into a global crisis will find a well-founded classification there.

If you want to understand the economic consequences of the pandemic, there is no getting around one fundamental question: How did it all begin? While this article deals with the effects on inflation, growth and economic forecasts, it is worth taking a complementary look at the origins of the virus itself. A separate article addresses precisely this point - objectively, calmly and without jumping to conclusions. It compares the various theories on the origins of SARS-CoV-2, from natural origins to laboratory hypotheses, without evaluating any of them one-sidedly. The aim is to provide orientation and the basis for making your own judgment. Precisely because economic developments were so strongly influenced by the first months of the pandemic, this review helps to better understand the overall picture. Anyone wondering how a local health report turned into a global crisis will find a well-founded classification there.

Sources used in the article

- Economics Network: Contribution to public perception of economic statements and confidence in economic forecasts.

- Peterson Institute for International Economics - Olivier BlanchardAnalysis from 2020 on why high inflation in advanced economies was considered unlikely, but not impossible.

- Office for National Statistics: Study on the impact of lockdowns on household spending and consumer behavior during the pandemic.

- Peterson Institute for International Economics: Illustration of how the pandemic has shifted consumer spending from services to goods.

Frequently asked questions

- What has made the pandemic so unreliable for economic forecasts?

The pandemic brought together several extraordinary factors at the same time - from global supply chain disruptions to government intervention and changes in consumer behavior. This combination was not sufficiently taken into account in many models. - Why were many economists wrong about inflation?

Many assumed that high unemployment and cautious consumer behavior would keep prices stable. However, the actual bottlenecks in production and logistics led to a sharp rise in prices. - What role did supply chains play in inflation?

They were a decisive factor. Production stoppages and transportation problems led to supply bottlenecks, which caused prices to rise significantly in many areas. - Why did inflation develop so differently from expectations?

Because several influencing factors acted simultaneously, including government aid programs, catch-up effects in consumption and global disruptions - a combination that rarely occurs in this form. - Why was the USA able to recover faster than many European countries?

The USA benefited from a more flexible labor market, extensive government support measures and less dependence on external shocks such as the energy crisis in Europe. - How important is the labor market for economic growth?

A flexible labor market makes it possible to react more quickly to changes. Employees can switch to growing sectors more easily, which accelerates the recovery. - Why was productivity partly overestimated during the pandemic?

Part of the increase was due to statistical effects, such as the closure of less productive sectors. This made overall productivity appear higher than it actually was. - What are so-called composition effects in productivity?

This shifts the structure of the economy so that more productive sectors become more important. This increases measured productivity without any real efficiency gains. - Has digitalization sustainably improved productivity?

In part, yes, but many effects were short-term. Long-term improvements depend on how permanently new working methods and technologies are integrated. - Why has the national debt risen so sharply?

Governments had to finance extensive aid programs to support companies, secure jobs and cushion economic slumps. - Is a high level of national debt fundamentally problematic?

It can harbor risks in the long term, but is often necessary in times of crisis to avoid major economic damage. - Which countries were particularly hard hit by rising debt?

Particularly countries with already high levels of debt or limited access to capital markets, such as in parts of Africa or East Asia. - What long-term consequences can debt have?

It can restrict future investments, lead to austerity measures or reduce governments' room for maneuver. - What is the most important lesson to be learned from the misjudgments of the pandemic?

That economic developments are more complex than many models can depict, especially in times of crisis with several factors acting simultaneously. - How should economic forecasts be improved in the future?

By taking greater account of uncertainties, alternative scenarios and a greater openness to different developments instead of overly rigid assumptions.